Car Insurance & Tuning in Germany: The €5,000 Recourse Trap

What happens when you don't disclose your tune to your insurer, what legal mechanisms apply, and why your liability stays valid for the victim — but the insurer comes after you.

May 6, 2026 by Leo Efimow

TÜV approval done, Stage 1 cleanly homologated, vehicle registration updated — only afterwards do many customers ask: "And my insurance, do I actually have to tell them anything?" The short answer: yes, promptly and in writing. The longer answer involves a legal construct that can quickly become more expensive than TÜV ever was: Gefahrerhöhung (insurance-law concept of "increased risk" under § 23 VVG, the German Versicherungsvertragsgesetz, or Insurance Contract Act). If you don't disclose your tune, you risk losing your Kasko (comprehensive) cover, and in a third-party-fault accident you can face classic recourse from your liability insurer — typically up to €5,000, in extreme cases far more. This article explains what happens legally, what makes practical sense, and why notifying your insurer is a core part of running a legal tune.

A Tune Is "Increased Risk" in Insurance Law

When the insurer underwrites your policy, it prices the risk based on what you provided: model, output, annual mileage, parking situation, who drives. If any of that changes after the contract starts, German insurance law calls it a Gefahrerhöhung — an "increase in the insured risk." § 23 VVG is explicit: the policyholder must not bring about an increase in risk after contract conclusion without informing the insurer. If they do anyway, the insurer can cancel the contract or adjust the premium — and reduce payout in the event of a claim.

A power increase through software or hardware tuning clearly falls under this rule. 184 hp becomes 230 hp, the acceleration profile changes, statistical accident probability rises — that's the logic an insurer applies. Whether the power increase is entered in the vehicle registration is a separate, road-traffic-law question. Notifying the insurer is the insurance-law question. Both have to be handled separately.

What Happens When the Tune Is Not Disclosed

This is where it gets expensive. The legal split is sharp and plays out on two levels — Kasko and Haftpflicht (mandatory third-party liability cover). Kasko insures your own car. If you don't report the increased risk and then suffer a loss on your own vehicle (theft, hail, at-fault accident), you risk full denial of cover by the Kasko insurer. Under § 26 VVG the insurer can be wholly or partly released from the obligation to pay if the unreported increase in risk caused the loss or was at least brought about by gross negligence (grobe Fahrlässigkeit, an explicit statutory category in German civil law).

Haftpflicht behaves differently. It protects accident victims — not the policyholder. To protect third parties, the liability insurer cannot refuse payment to the injured party even if the policyholder concealed the tune. It pays the victim as agreed in the policy. The catch: it can then turn around and pursue Regress (recourse — the insurer's statutory right to recover from its own policyholder) against you.

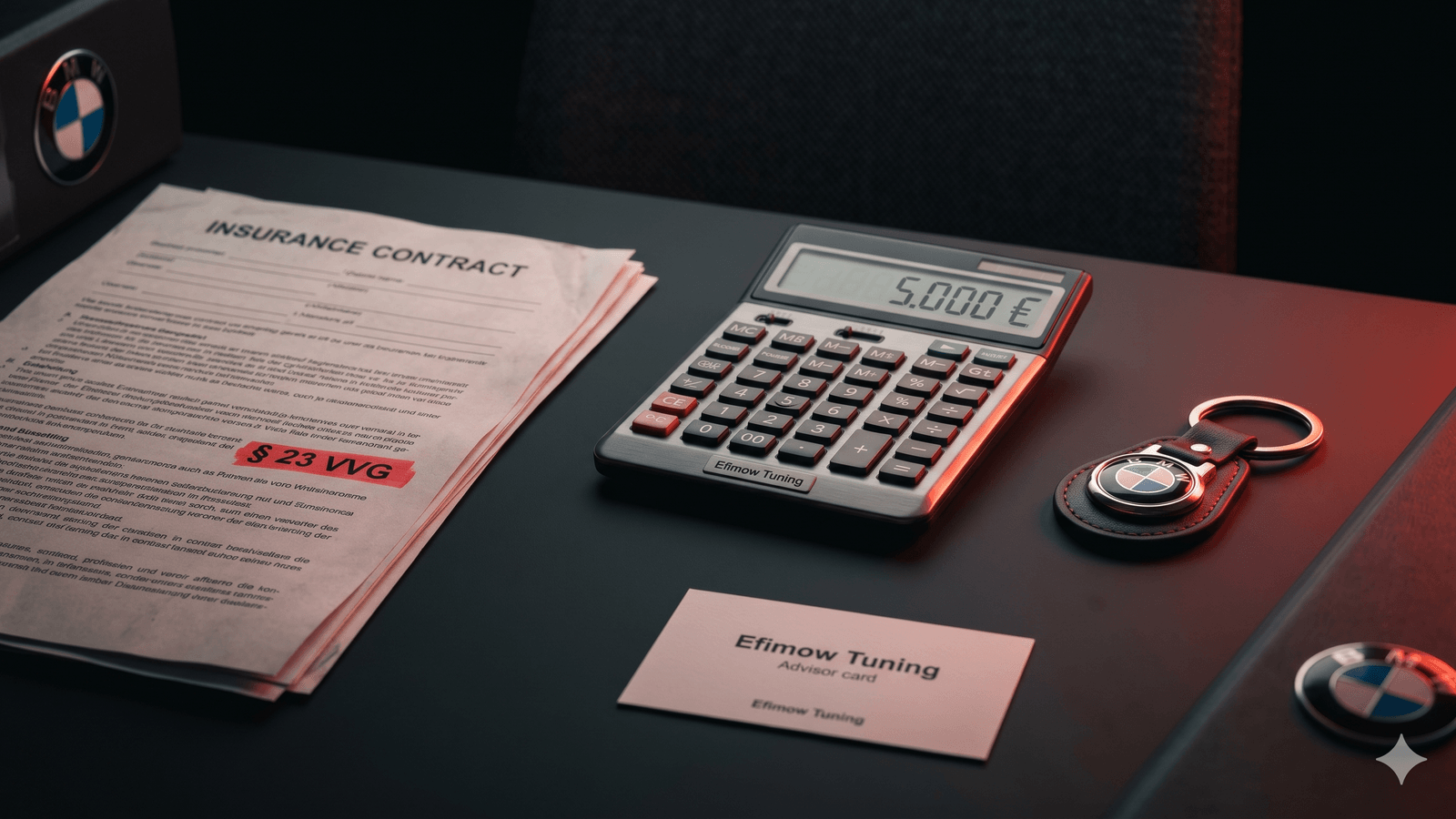

Recourse: Typically up to €5,000, Theoretically Unlimited

Recourse is the trap many tuners underestimate. If the policyholder breached an Obliegenheit (a contractual duty owed to the insurer) — i.e. violated the disclosure obligation under § 23 VVG — the liability insurer can, under § 28 VVG, recover part or all of the claim payment from its own policyholder. With most German insurers this recourse is contractually capped at up to €5,000; that's industry standard and is normally written into the AKB (Allgemeine Bedingungen für die Kfz-Versicherung, the general terms for motor insurance in Germany).

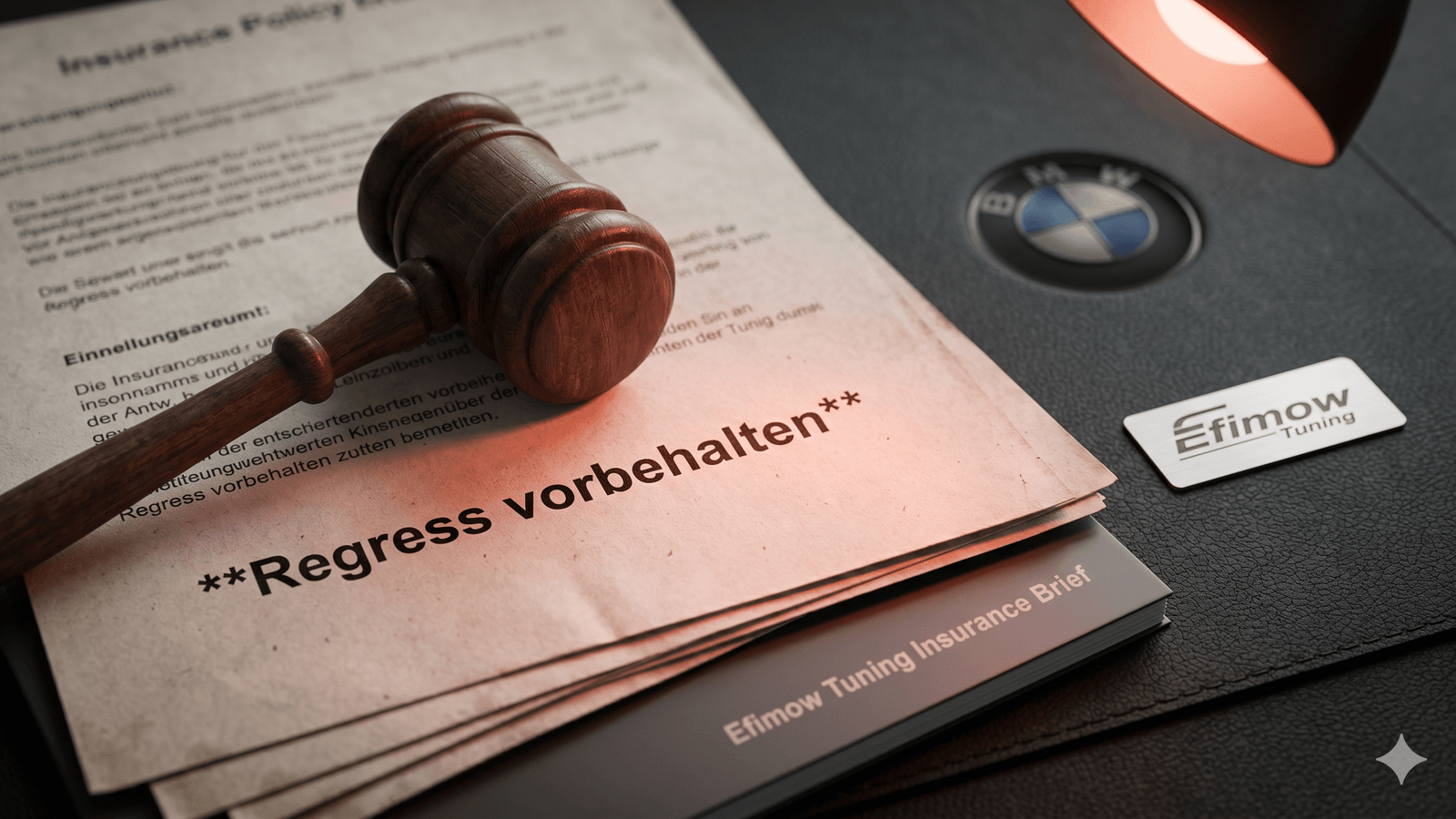

In theory, recourse can run higher. In cases of grobe Fahrlässigkeit or outright Vorsatz (willful intent) — say, a clearly tuned car deliberately not reported, with the tuning character contributing to the accident — the insurer can pierce the contractual cap. With a personal-injury claim and a high settlement, that means six-figure exposure in extreme cases. BGH (Bundesgerichtshof, Germany's federal civil supreme court) case law isn't fully uniform here, but it includes enough decisions where insurers succeeded with elevated recourse claims — particularly when the tune was safety-relevant (brakes, suspension, tires) or when the power increase plausibly shaped the accident.

What a Proper Notification Actually Looks Like

The notification itself is refreshingly unspectacular. As a rule, a brief written message with the basics is enough: which vehicle, which modification, the new power figure, and the TÜV reference (Teilegutachten, ABE, or Einzelabnahme under § 21 StVZO, Germany's road-traffic licensing regulation). Most insurers add a form or ask for a copy of the TÜV approval. Processing usually takes a few days. Three reactions are possible.

First: the insurer accepts and adjusts the premium — usually a moderate surcharge depending on added power and tariff. For a 184-to-230 hp Stage 1 on a G20, a surcharge of 5–15 % is typical. Second: the insurer accepts in principle but asks for additional documentation or an inspection. Third: the insurer declines to cover the modified state under the existing tariff. In that case the policyholder has a statutory Sonderkündigungsrecht (special right of cancellation) and can switch to a tuning-friendlier provider — important: with no coverage gap.

Deadline, Switching, and the Most Common Mistake

The most common mistake isn't deliberately concealing the tune — few people do that. The most common mistake is dragging the notification out. § 23 VVG requires the disclosure to be made "unverzüglich," a German legal term meaning "without culpable delay." A sensible practical rule is to notify the insurer within two weeks of TÜV approval. Waiting several months exposes you to problems even if the modification would have been insurable in the first place.

Two further points matter. First: a hardware modification not yet activated in software (e.g. an installed downpipe with no calibration change) is not legally unambiguous — to be safe, ask the insurer in writing. Second: if you switch insurers because the previous one doesn't cover tuned vehicles, conclude the new contract with honest disclosure of the tuned state — otherwise you recreate the same disclosure breach with the new insurer.

Bottom Line

Legally, the situation is clear: a tune is a Gefahrerhöhung, the disclosure obligation is unambiguous, and recourse under § 28 VVG is real. If you notify your insurer promptly and correctly, the worst case is a premium surcharge or a switch of carrier — both manageable. If you stay quiet, you risk losing your Kasko cover after a claim and facing a recourse claim that, on standard tariffs, runs up to €5,000 — and far higher in cases of gross negligence or willful intent. Tuning entered in the registration plus tuning declared to the insurer is the only combination that holds up over time.